3 Resolutions for Your DC Plan in 2025

Paula Smith

Senior Vice President, Head of DC and College Savings Products

New features may not be what your plan needs this year. There’s plenty to be gained from simply refining what already works.

Many New Year’s resolutions are made from a deficit mindset: What’s wrong, what’s lacking, what needs to be fixed. It’s not surprising, then, that few people actually stick to them throughout the year.

A better approach may be to build on existing strengths and incrementally improve on what’s already working for a higher chance of success. This method isn’t just useful for personal goals—it can help DC plan sponsors, too. So here are three ideas to consider in 2025.

1 Revisit auto features

Auto features are among the most effective tools for helping workers save for retirement. For example, auto-enrollment is great at boosting participation—but it doesn’t ensure participants are saving enough. The problem is that once enrolled, participants tend to stick to the default contribution rate. Get them off to a better start on their retirement journey by setting a higher default rate, such as 7%. Voya’s proprietary research shows that participants tended not to opt out of auto enrollment even when the default rate was close to 10%.1

Once they’re enrolled, help participants fight inertia by enabling auto-escalation. Increasing the savings rate by 2% per year, up to 15% of salary, can help them be better prepared to meet their retirement goals.

If the plan has introduced new investment options (such as TDFs), conducting a re-enrollment may help long-time participants get back on course. This involves reallocating existing account balances and future contributions from their current investment allocations to the plan’s QDIA, unless participants opt out. Re-enrollment can help move participants to more appropriate asset allocations based on their age and retirement timeline if they’ve drifted away from them over time.

2 Re-evaluate your QDIA

Among 401(k) plans that have a QDIA, 78% use an off-the-shelf target date fund.2 We’ve observed many sponsors’ tendencies to select passive TDFs, largely because of their low costs. However, three things often go overlooked in this decision:

- Passive TDFs aren’t actually passive. Unlike index funds that track a benchmark such as the S&P 500 or the Nasdaq, passive TDFs involve many active decisions, such as glide path construction, portfolio construction, asset allocation and the choice of “to retirement” or “through retirement” landing points. These decisions by the manager can lead to a wide variation in outcomes.

- The fee difference with active TDFs is often negligible. The average fee difference between a passive and a blended TDF is about 30 basis points. But the return dispersion can be much wider given significant differences in investment philosophies and approaches.

- Choosing passive doesn’t automatically protect sponsors from getting sued. The truth is that litigation related to investment underperformance and fiduciary imprudence has increased in recent years.3

A suite of blended TDFs that combine active and passive underlying investments may be an effective middle ground. Such TDFs may seek to add value by using active strategies in less efficient asset classes such as fixed income and alternatives, where active management has historically had a higher likelihood of success. They balance this with passive strategies in more efficient areas, such as U.S. large cap equity, helping to keep overall portfolio costs down. Blended TDFs typically offer broader asset-class diversification, consisting of more than twice as many underlying categories as passive TDFs on average. DC plan consultants are also more likely to recommend a blended TDF series compared with active or passive alternatives.4

Blended TDFs that combine active and passive management may improve diversification and long-term outcomes net of fees.

Whichever type of TDF suite you choose, make sure you have the right educational tools. Research from EBRI/ICI shows that participants in their 60s are less likely than their younger counterparts to invest in TDFs5—possibly because they started saving before these vehicles were introduced. Ensure resources are available to help employees understand that TDFs are a one-stop solution, offering a diversified and professionally managed portfolio that maintains an appropriate level of risk based on the target date. And if the target date suite includes a retirement income vintage—promote it! Older participants who take a DIY approach to investing may have a higher-than-ideal allocation to equities.6

Reviewing fiduciary responsibilities to ensure reasonable investment fees can help enhance participant outcomes.

Many sponsors of larger plans are also re-considering implementing custom TDFs given their many benefits, including their ability to tailor the investment strategy to the specific needs of a participant population, greater adaptability and a higher likelihood of better participant engagement. Custom TDFs also allow for specific incorporation of retirement income strategies for participants.

3 Review fiduciary responsibilities related to the investment menu

One aspect of a sponsor’s role as fiduciary is to review investment fees to ensure they are reasonable. Sometimes this means selecting lower-cost share classes or investment vehicles for the plan if available. But sponsors aren’t obligated to pick the cheapest option or offer only low-cost passive options in the plan. The focus on the value an investment offers relative to its cost.

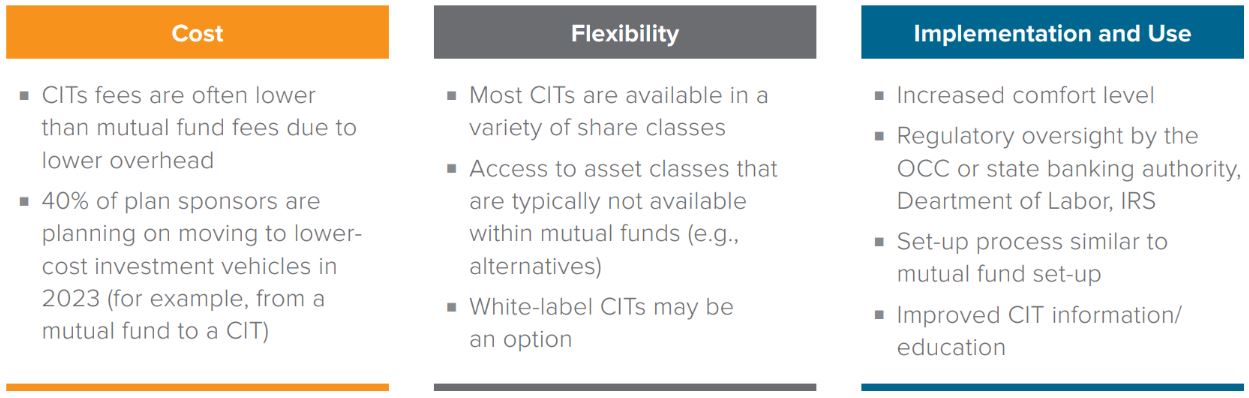

One low-cost vehicle to consider way is the collective investment trust (CIT). These bank-regulated investment vehicles generally behave like mutual funds, but with lower fees. Although CITs aren’t registered with the Securities Exchange Commission, they are subject to numerous laws and regulations imposed by federal and state banking regulators, the Department of Labor, the Internal Revenue Service and, in some cases, FINRA. See our short paper on CITs here.

A note about risk

There is no guarantee that any investment option will achieve its stated objective. Principal value fluctuates and there is no guarantee of value at any time, including the target date. The “target date” is the approximate date when an investor plans to start withdrawing their money. When their target date is reached, they may have more or less than the original amount invested. Stocks are more volatile than bonds, and portfolios with a higher concentration of stocks are more likely to experience greater fluctuations in value than portfolios with a higher concentration in bonds. Foreign stocks and small- and mid-cap stocks may be more volatilethan large-cap stocks. Investing in bonds also, entails credit risk and interest rate risk. Generally, investors with longer timeframes can consider assuming more risk in their investment portfolio.